BHPW Newsletter Q4 2025

MARKET RECAP

Despite a few brief flare-ups, global equities marched higher during the final quarter of 2025, with gains broadly distributed across regions and sectors. The MSCI All Country World Index (“ACWI”) rose +3.3%.

That result capped a third consecutive strong year for equity investors, with the ACWI returning +22.3% for the full year. International markets delivered an especially robust performance, rising +31.2% compared with the S&P 500’s +17.9%.

Yet those year-end results tell only part of the story. The path to reaching them was anything but easy.

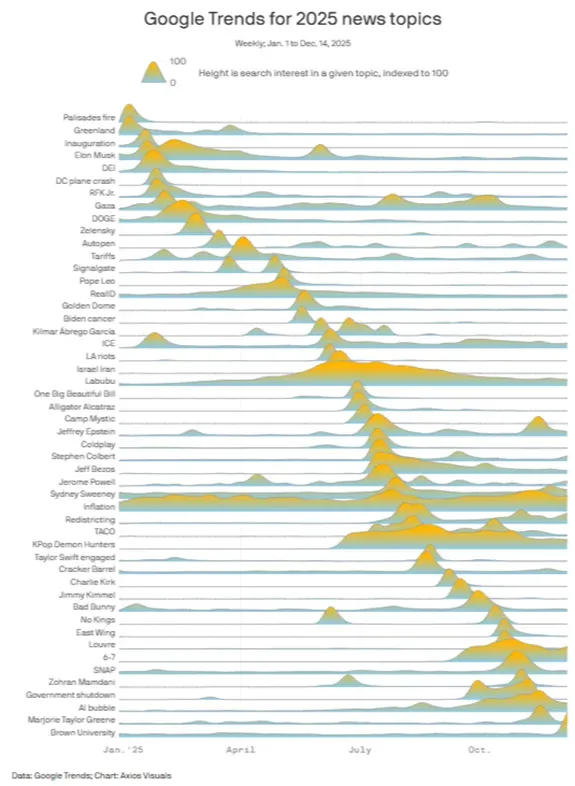

Throughout 2025, investor attention was repeatedly pulled from one major issue to the next. The chart below captures that unusually broad mix of themes, which spanned politics, geopolitics, inflation, the economy, and even cultural moments. Not every headline moved asset prices, but the cumulative effect was still a year marked by frequent shifts in focus.

The most consequential market episode came in April, following the US tariff announcements. Equities sold off sharply, briefly falling nearly -20% from their highs. This reaction ultimately proved short-lived, as several of the most severe tariff scenarios were walked back and the anticipated second-order disruptions failed to materialize. Even so, the episode served as a clear reminder of how quickly investor sentiment can change.

In contrast, bonds followed a steadier course throughout 2025, largely insulated from the headline-driven volatility. Returns were positive in each quarter, and the Global and US Aggregate Bond indices climbed by +8.2% and +7.3%, respectively. Both benefited from falling interest rates, which lifted bond prices.

BHPW PERFORMANCE

Against this backdrop, BHPW portfolios delivered strong results in 2025.

Within equities, we slightly trailed the ACWI’s +22.3% but meaningfully outperformed the S&P 500’s +17.9%, aided by strong contributions across a broad set of holdings.

That breadth exceeded our expectations. As we’ve noted in prior letters, in a typical year only about two-thirds of equity holdings are likely to be “working” – that is, generating positive returns. We cleared that bar once again last year, with roughly 75% of holdings finishing in the green.

Equally important was the strength of the winners relative to the losers. Out of 84 model securities held throughout the year, only six declined by -25% or more, while thirty-five gained +25% or more. Many of those winners have been compounding in our portfolios for years, reinforcing a core investing truth: you make money with old friends.

That said, strong years shouldn’t invite complacency. Some of our winners have grown more expensive in valuation, while laggards risk becoming value traps. We continuously underwrite and re-underwrite our holdings to ensure each remains on the right long-term track. That’s especially important for the names that are underperforming.

Thankfully, in the case of the six names that experienced larger drawdowns, we continue to like what we see: market-leading franchises, structurally growing industries, and valuations we deem attractive at just 12.8x earnings on average. These companies may be out of favor today, but sentiment can turn quickly. To that point, they are already up an average of +5% in the first ten trading days of the year.

Meanwhile, in fixed income, our bond models performed as intended. Nearly every security finished with gains, and while returns slightly trailed the bond benchmarks, they still exceeded +7% for the year. We’re comfortable with this outcome given our conservative positioning across credit and duration – a trade-off we view as prudent in today’s environment.

MANAGING THE DOWNSIDE

One result particularly stood out last year. Our equity portfolio’s downside capture ratio – which measures what percentage of the market’s downside we experienced on down days – was negative, at roughly -11%. In practical terms, that means on days when the market declined, our equity portfolios generated positive returns on average.

We view this outcome as largely a function of today’s market structure. As we’ve highlighted recently, indices have become increasingly concentrated in a narrow set of mega-cap and technology holdings. In contrast, we believe our portfolios are actually more broadly diversified, at least across sectors, geographies, and risk factors. In an environment where down days are often driven by a small subset of forces, our diversification creates the room to hold up better than the market.

We don’t expect a negative downside capture to be the norm. But since inception, our in-house BHPW equity models have delivered a resilient downside capture ratio of roughly 61%. In fixed income, that figure has also remained below 20% relative to its comparable bond benchmark. Together, these results point to meaningful protection for our portfolios during periods of market declines.

We think of this protection as the “sixth man” of our philosophy – quietly important in normal times, but especially essential when conditions turn prolonged for the worse. That feels particularly relevant today as we navigate elevated market conditions.

LOOKING AHEAD

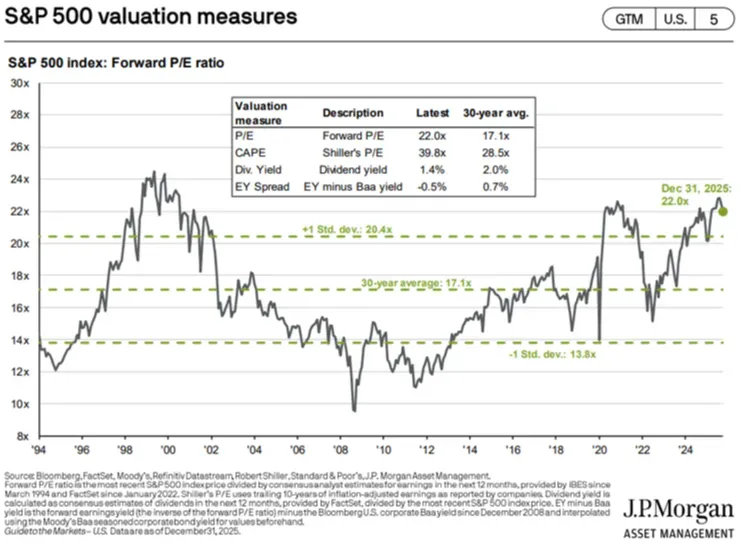

At roughly 22x forward earnings, the S&P 500 is now hovering near its most expensive levels. The only two other periods with higher valuations were 1999 and 2021. As many readers will recall, both were followed by challenging market environments for investors.

Rather than treating valuations as a binary signal – black or white – we think of them as gray. After all, expensive markets can still deliver returns in line with fundamentals, driven by dividends (roughly 1.5% today) and earnings growth (historically in the 5%-6% range).

At the same time, two dynamics are worth keeping in mind at these levels. First, generating additional returns from multiple expansion becomes increasingly difficult. Second, drawdowns tend to be more severe when starting from a higher base.

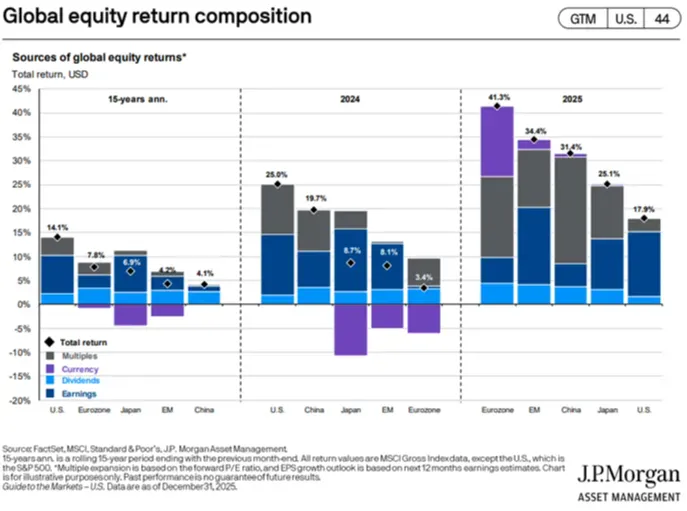

We can illustrate the first dynamic by breaking historical market returns into their components. As the chart below shows, the strong results in 2024 and 2025 were driven in large part by multiple expansion (dark gray). Over the long run, however, this tends to even out, with returns gravitating back toward their underlying fundamentals (the dark and light blue bars in the 15-year section). With valuations already above their historical ranges, we don’t expect a lot more positive dark gray surprises.

Note: This 15-year period begins from the post-crisis trough in 2010, when both earnings and valuation multiples were depressed.

This amplified the subsequent contribution from earnings growth and multiples normalization.

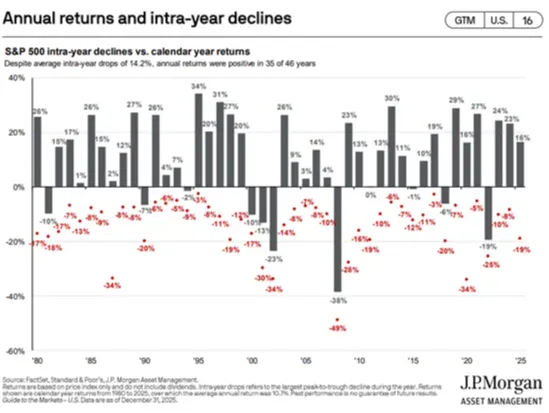

Meanwhile, the chart below highlights how higher valuations tend to amplify drawdowns. Since 2020, valuations have remained above average, and intra-year drawdowns have been correspondingly deeper, averaging roughly -17% per year. From 2011 to 2018, when valuations were generally lower, drawdowns were closer to -10%.

What this means to us: looking at today’s index levels, there’s a reasonable chance we revisit them at some point later this year.

BHPW POSITIONING

Richer valuation environments increase the importance of portfolio construction and diversification.

If you woke up tomorrow having won a $100 billion lottery, you wouldn’t allocate a meaningful portion of it to a single stock trading at 200x earnings – a 0.5% earnings yield. Nor would you anchor your future to one company, one sector, or one narrative, no matter how compelling it may seem. Instead, you would build a balanced portfolio with diversified exposures across multiple risk factors, designed to endure a wide range of possible outcomes.

For decades, index funds served as a reasonable proxy for that diversification. But that benefit has quietly eroded over time, as the top ten names in the S&P 500 now represent more than 40% of the index. Technology, broadly defined, also accounts for roughly half of the exposure. What’s historically been a diversified fund is increasingly behaving like a concentrated bet.

That concentration matters. When exposures are narrow, portfolios become more vulnerable not only to earnings disappointments, but also to exogenous shocks. A geopolitical flashpoint, regulatory shift, or disruption in global supply chains can reverberate far more violently through today’s indices than many investors appreciate.

Our approach at BHPW is intentionally different. Rather than owning the whole market in proportion to its size, we focus instead on building high-quality portfolios driven by a broad set of economic drivers. We also emphasize disciplined valuation standards. The goal is not to avoid risk – that’s neither possible nor desirable – but to ensure risk is spread across multiple, independent sources of returns.

Viewed in aggregate, the result is a portfolio we estimate trades at a meaningful discount to both the S&P 500 and the ACWI. In an environment where concentration risk is increasingly embedded within these passive solutions, we believe thoughtful positioning like ours matters more than ever.

The objective remains the same as it has always been: build portfolios that can compound over time without excessive exposure to any single risk factor. We just believe our portfolios are better positioned in today’s market structure, given the risks inherent in many passive approaches.

CONCLUSION

We remain constructive on equities over the long run. However, markets rarely move in straight lines, and when sentiment turns, our focus will be on protecting client capital while positioning to participate in the next phase of compounding. We’ll remain disciplined and vigilant in that process.

At the same time, opportunities still exist across equity markets, and we believe most clients should maintain exposure to the asset class. That said, those positioned at the higher end of the equity spectrum – such as 90% or 100% allocations – may want to consider rebalancing modestly at the margin. Fixed income continues to offer attractive risk-reward, serving not only as a stabilizer but also as dry powder for future opportunities.

On a firm-level, 2025 was a milestone year for BHPW. We welcomed several new employees to our team and are on pace to surpass $1 billion in assets under management soon. We view this growth as a reflection of both our solid investment results and the trust our clients place in us.

We also ramped up our inaugural private fund, BHPW Select Opportunities Fund I, and completed a successful first year of allocations. Investors in that vehicle can expect an update in April.

Overall, we are deeply grateful for the confidence our clients place with us, and we remain committed to earning it every single day.

Beverly Hills Private Wealth, LLC is a registered investment adviser. This is solely for informational purposes. No advice may be rendered by Beverly Hills Private Wealth, LLC unless a client service agreement is in place. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful. Past performance does not guarantee future results. Investing involves risk, including loss of principal. Consult your financial professional before making any investment decision. Other methods may produce different results, and the results for different periods may vary depending upon market conditions and portfolio composition. This newsletter does not represent an offer to buy or sell securities.