BHPW Newsletter Q3 2025

MARKET RECAP

Stocks climbed higher throughout the third quarter, gaining +7.6% to reach new all-time highs. It was a surprising outcome, as investors looked past a long list of concerns – including tariffs, global tensions, slowdown fears, and a looming government shutdown – to keep the momentum going. That strength has lifted global equities +18.4% through the first nine months of the year.

Breaking it out by region, international markets continued to lead the way, rising +26.0%, while the S&P 500 posted a more modest gain of +14.8%. A weaker US dollar explains much of that gap, as its -10% decline has provided a meaningful boost to foreign assets this year.

Fixed income also added to the gains, with global bonds rising +0.6% for the quarter. That brings their year-to-date return to a solid +7.9%, helped again by the softer dollar. But even domestic bonds have delivered strong results, with the US Aggregate index up +6.1% this year.

Our portfolios performed well in this environment, with returns landing between our global and US benchmarks. On the equity side, we benefited from our overweight to international markets, although that strength was offset by our lower weighting in technology. Meanwhile, our bond models largely tracked the US Aggregate, keeping us on pace for a strong full-year performance.

Importantly, our portfolios have achieved these results while continuing to demonstrate resilience during market pullbacks. That’s been especially true for our equity sleeve, which has declined by less than half as much as the market on down days this year – resulting in a downside capture ratio of just 42%. Our bond models have shown similar resilience, capturing only about 15% of the downside in that category.

Protection remains central to our approach – and we think that’s especially important as we enter a period of rising uncertainty and stretched valuations. More on each of these below.

RISING UNCERTAINTY

More than ever, it feels like the rules of the game are shifting. Each week seems to bring new tariff threats or policy pressures – from recent actions targeting China and heavy-duty trucks to new government initiatives aimed at lowering drug prices. In this environment, predictability is becoming harder to find. Many of the business and economic frameworks that have guided us for decades are now being forced to adapt.

For example, from a traditional macroeconomic lens, we continue to believe that locking in high-quality bond yields above 5% remains compelling. The Fed is expected to cut interest rates twice more this year, which would bring short-term rates down to around 3.6%. In that context, locking in those higher rates should become increasingly attractive for investors.

But this time, a new and competing narrative is also taking shape. The US dollar is down by double digits, and gold continues to reach new all-time highs – suggesting that a broader diversification away from the dollar may already be underway. If trade and policy uncertainty push investors away from US assets more broadly, interest rates could begin to move in ways that defy the usual playbook.

We’re staying mindful of these crosscurrents, and our best defense remains diversification – avoiding big bets unless the odds are clearly in our favor. In bonds, that means gravitating toward a duration profile that can benefit from falling rates without meaningfully hurting us if they rise. In equities, it means broadening exposures as long as expected returns remain attractive. This discipline helps us avoid overreacting to every headline – which matters, since most tend to reverse just as quickly as they emerge.

In markets that keep rewriting the rules, staying diversified remains an advantage.

STRETCHED VALUATIONS

It’s also becoming harder to ignore the euphoria building in parts of this market. By our estimates, trillions in market value now rest on optimistic assumptions – a meaningful figure by any standard. Many of those areas are just one disappointment away from sharp pullbacks.

Even among blue-chip names, valuations are starting to look stretched. We wrote about JPMorgan in our Q4 2023 letter, describing it as a best-in-class company trading at a 10% earnings yield. Less than two years later, the stock is up roughly +90%. While part of that reflects genuine earnings growth, valuations are about 50% higher now than they were back then – leaving far less margin for error.

The same is true for other blue-chip names. Even if a company like Costco executes flawlessly from here, the stock may still deliver only modest returns. At 40x earnings, perfection is priced in – and even small missteps could lead to stagnant or negative results.

In many areas, we’re seeing 40x earnings – or higher – increasingly treated as the norm. And while some companies may justify those valuations, many likely do not. Fortunately, opportunities that meet our standards still exist across this market, and we remain selective in pursuing them.

BHPW POSITIONING

Staying diversified and selective doesn’t mean standing still. Here’s how we’re positioning for the road ahead.

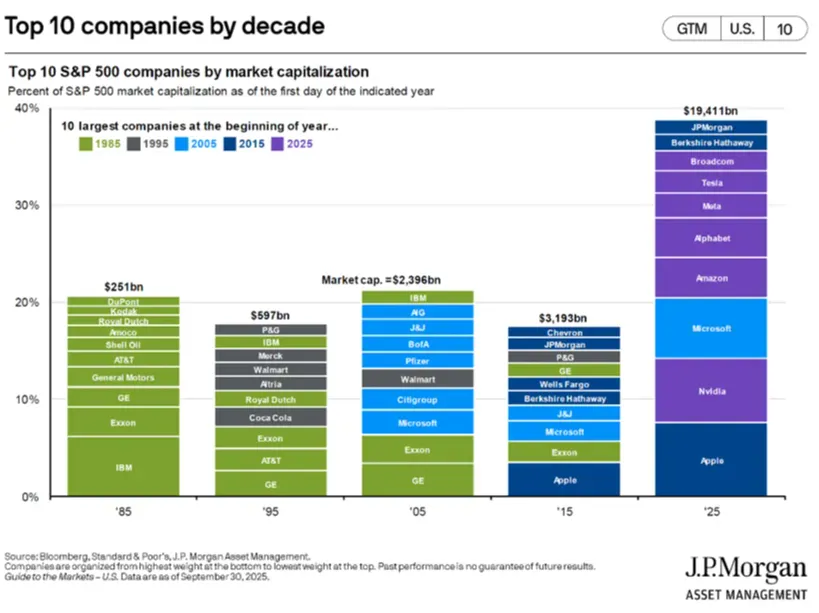

On the equity side, we continue to lean away from the more crowded areas of the market. Nearly 45% of the S&P 500 is classified as Technology or Technology-adjacent, and the 10 largest companies account for almost 40% of the index. That’s unusually concentrated leadership – as the chart below shows – and the companies at the top rarely stay there for very long. Historically, at least half of the top ten US stocks have turned over every decade.

AI will no doubt change the world and drive major productivity gains – just as the internet, automobiles, and railroads once did – but the eventual winners are rarely the ones trading at the highest prices. Many companies will benefit, but far more will be disrupted than the market currently expects.

Instead of chasing what’s already worked, we’re finding value in the less crowded corners – particularly in international and smaller US companies. One recent purchase is an Ohio-based bank offering a 9% dividend yield that we believe will soon move higher. It’s a company we’ve followed for more than a decade, and it’s been written off in recent years after overextending into low-rate mortgages. That chapter now appears to be turning, and earnings momentum should improve meaningfully from here.

Opportunities like this arise in every environment, and capturing even a few each year helps us navigate equity markets more effectively.

Meanwhile, in fixed income, we continue to favor moderate duration and conservative credit exposure, which gives us flexibility if conditions change unexpectedly for the worse. We’ve already begun to see early signs of stress among certain private-credit issuers. Many of these unconventional lenders have enjoyed a long run with limited stress testing, and a genuine downturn could expose vulnerabilities lying beneath the surface. While no major issues have emerged so far, we’re prepared to act opportunistically when spreads eventually widen.

In the meantime, we’ve continued adding to a handful of harder-to-trade bonds that offer strong value – often earning two percentage points or more above Treasuries for predominantly investment-grade issuers. The biggest challenge is simply sourcing them in meaningful size.

CONCLUSION

While uncertainty has been rising, our portfolios remain well positioned for it – diversified across exposures, high in credit quality, and intentionally avoiding over-concentration. And while parts of the market look extended, opportunities still exist for those willing to stay selective and grounded in fundamentals.

In the absence of a major shock, we expect equities to move higher, supported by solid earnings growth and gradually improving sentiment. And despite our somewhat cautious tone, we continue to see room for attractive returns ahead – which we define as solid double-digit potential in equities and mid-single-digit yields in bonds.

Our focus remains on delivering those results while maintaining the same discipline and downside protection that have served us well through past bouts of volatility.

As always, we appreciate your trust and confidence.

Beverly Hills Private Wealth, LLC is a registered investment adviser. This is solely for informational purposes. No advice may be rendered by Beverly Hills Private Wealth, LLC unless a client service agreement is in place. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful. Past performance does not guarantee future results. Investing involves risk, including loss of principal. Consult your financial professional before making any investment decision. Other methods may produce different results, and the results for different periods may vary depending upon market conditions and portfolio composition. This newsletter does not represent an offer to buy or sell securities.