BHPW Newsletter Q1 2026

MARKET RECAP

Markets took a turn for the worse to start 2026, with global stocks declining -3.2% in the first quarter. The S&P 500 fared even worse, falling -4.3%, while bonds also failed to provide relief, with the Global Aggregate index down -1.1%.

At the center of all these moves was the escalation in the Iran conflict, which began in late February and has weighed on markets ever since. Energy was the first to react, with crude oil and global natural gas prices surging more than 75%. These pressures quickly moved downstream into fertilizers, agricultural commodities, and other energy-intensive inputs.

In turn, rising inflation expectations pushed interest rates higher, bond prices lower, and equities toward correction territory.

Against this backdrop, our BHPW portfolios held up well, with both our stock and bond models finishing the quarter in positive territory. In equities, performance was supported by our international diversification, defensive positioning, and energy exposure, though this was partially offset by weakness in technology and consumer discretionary.

In fixed income, we benefited from our security selection and shorter duration profile, though we did experience some headwinds in longer maturities.

DOWNSIDE DISCIPLINE

Last quarter, we referred to downside protection as the “sixth man” of our process – always important, but often overlooked. It showed up last year during the tariff-driven selloff, when our equities were down roughly half as much as the broader market. And it showed up again this quarter, with our portfolios capturing approximately 63% of the downside in stocks and 53% in bonds. In practical terms, that means on down days, our portfolios declined meaningfully less.

A client recently asked how we achieve this. At a high level, it comes down to intentional design. We are willing to walk away from a riskier 15% annual return for a more durable 13% outcome. We also build our portfolios with the expectation that not everything will go right, actively stress testing across a range of adverse scenarios. Our allocation to energy this period – focused on long reserve life producers in stable jurisdictions – was partly the result of planning with environments like this in mind.

If markets continue to move lower, we feel well positioned. In equities, we view nearly half of our exposure as recession resilient. Meanwhile, in fixed income, our largest holdings – representing ~71% of the allocation – are either AAA, government-backed, or high-grade municipals.

We are long-term optimists, but recognize that more severe drawdowns than this are inevitable. After all, many of the worst single days in market history have seen declines far greater than anything we’ve experienced so far. Our job is not to predict exactly when those days will occur, but to be prepared when they do.

ELEVATED EXPECTATIONS

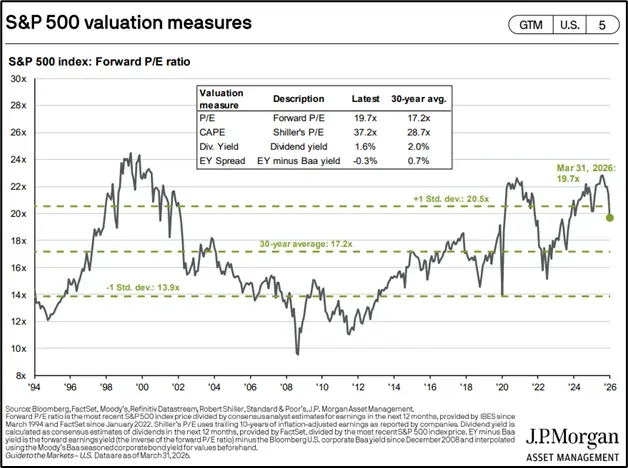

With the recent market pullback, valuations have moved back within their historical range. That said, they remain at the higher end of those norms, at a forward P/E multiple of 19.7x versus the long-term average of 17.2x – and the BHPW model at approximately 13x.

Compounding matters, we believe the earnings expectations underlying those market multiples are too ambitious. Consensus estimates still call for the S&P 500 to grow earnings by roughly 18.5% annually over the next two years. Against a backdrop of slowing labor demand, rising energy costs, and ongoing geopolitical tension, that appears optimistic.

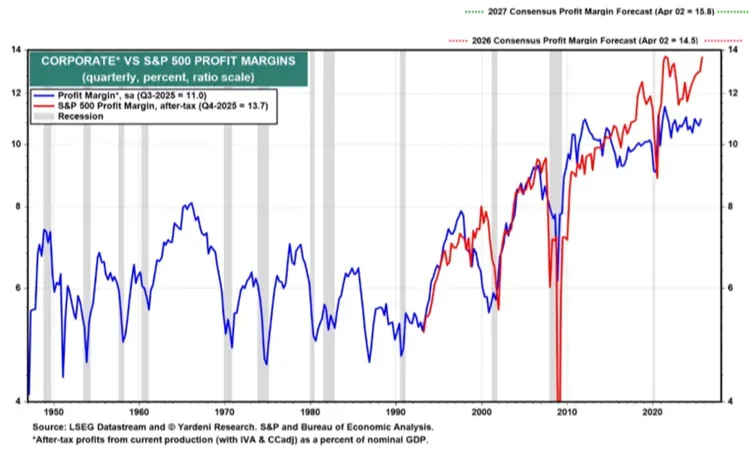

The chart below highlights one inconvenient implication of that forecast. If the market were to meet its current EPS expectations, implied profit margins for 2026 and 2027 would be, quite literally, off the charts – well beyond anything seen since the 1940s.

Taken together, elevated valuations are supported by stretched earnings estimates. Even after the recent pullback, markets look moderately expensive to us.

SOFTENING SUPPORT

Meanwhile, cracks are beginning to form in the economic backdrop.

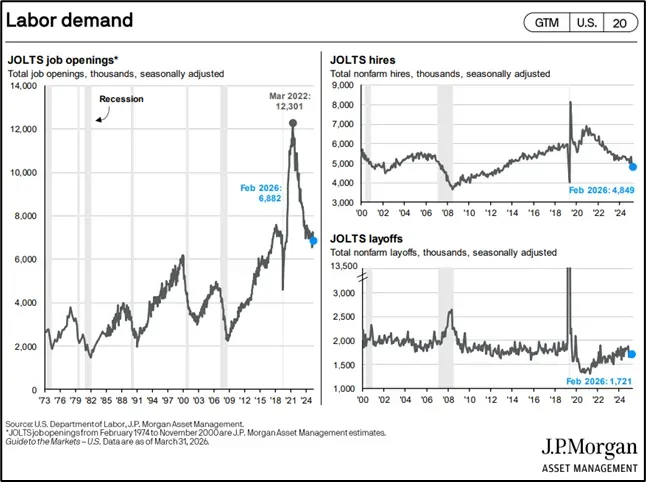

For much of this cycle, our view has been that the economy is on stronger footing than many were willing to give it credit for. The reasoning wasn’t overly complex: as long as job openings remained significantly elevated, we believed the economy would remain resilient. The chart below highlights the surge in openings that began shortly after COVID.

It was difficult to imagine a severe recession with more than ten million jobs available. However, that support is now fading, with the latest JOLTS data pointing to slower hiring, rising layoffs, and openings back at 2018 levels.

If a shock were to hit the economy today, we would no longer have the same labor market cushion.

CONSUMER CONTRAINTS

At the same time that the employment picture is becoming more uncertain, the consumer is also becoming more fragile.

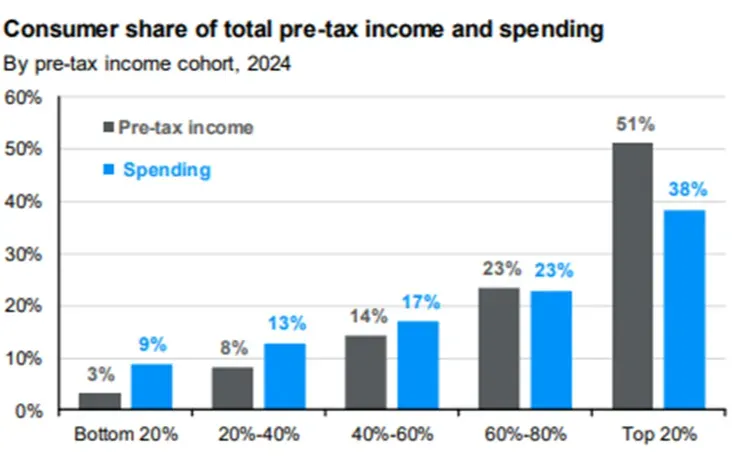

The chart below shows income and spending across 20% income cohorts. Two things stand out. First, the bottom 60% of earners are spending more than they earn. Second, the top 20% account for a disproportionate share of consumption.

More than focusing on this current state of affairs – often referred to as a K-shaped economy – we are concerned with the second-order implications. Much of the population appears constrained and poorly equipped to absorb a shock. At the same time, any slowdown among higher earners could have an outsized impact on overall activity.

Combined with the weaker employment backdrop discussed earlier, we believe the economy is more vulnerable than it has been in years.

AI ANXIETY

Could AI be the catalyst that exposes those vulnerabilities?

We’ve been asked this increasingly in recent months, and while we don’t claim to have a crystal ball, we are somewhat more optimistic here.

Periods of technological change tend to reshape industries rather than eliminate them, and the impact is often more gradual than expected. Driverless cars exist today, yet they have done little to change our day-to-day habits. TurboTax didn’t eliminate accountants; self-checkout didn’t replace cashiers; Zoom didn’t end business travel.

We expect AI will follow a similar path, and to the extent displacement occurs, the more immediate effect is likely to be a reallocation of labor and capital rather than a reduction. After all, AI is highly capital intensive, requiring significant investment in infrastructure, compute, energy, and skills – spending that is inherently supportive of growth.

The distribution of profits may shift, but we would expect the overall pool to grow – with the rising tide of AI lifting much of the economy.

WAR WATCH

No letter would be complete without addressing the current Iranian conflict.

As we noted in our March update, we view a prolonged escalation as unlikely, given the significant economic incentives for a swift resolution. Energy markets in Europe and Asia are already under heavy pressure, which should reinforce a global push toward stability.

That said, the environment still carries elevated uncertainty, and there are views we respect suggesting the conflict could persist longer than anticipated. One of the key risks is that the primary parties involved do not want to be seen as conceding, which could prolong the path to resolution.

While this may lead to a more uneven trajectory, we still believe resolution remains the most likely outcome. If that proves to be the case, we would expect the broader economy to revert toward its earlier pace of growth.

BHPW POSITIONING

Given the current environment, how are we positioning portfolios for the road ahead?

In equities, we remain firmly anchored to our core tenets, seeking to own high-quality businesses that often trade at valuations we feel offer meaningful downside protection. This is reflected in the portfolio’s valuation of approximately 13x earnings, well below broader market levels. Position sizing remains measured as well, ensuring no single outcome can materially impair performance.

We also continue to find mispriced opportunities, with two recent additions illustrating this. In March, we added a high-quality multifamily REIT at what we estimate to be a nearly 8% free cash flow yield. We also initiated a position in a large US asset manager where a meaningful portion of the purchase price is backed by cash and investments on its balance sheet. This implies the core operating business trades at just 3-4x normalized pre-tax earnings.

Elsewhere, in fixed income, we are maintaining a defensive posture while selectively leaning into higher-yielding opportunities.

On one end, we have been adding to A-rated, long-term securities yielding between 6.3%-7.0% – levels at which we feel comfortable locking in duration. On the other, we have also been initiating smaller positions in dislocated credit opportunities that have been overly penalized. Many of these offer yields of 8% or more to our expected exit.

One of these positions has ties to private credit, and we are not surprised to see greater scrutiny at this stage of the cycle, as this is the type of stress we would expect as the expansion matures. While we have largely avoided the space until now, we recently initiated a position in a publicly traded business development company at approximately 67% of book value. That discount creates a compelling entry point.

CONCLUSION

Market pullbacks often create attractive opportunities to add to exposure, and we expect this period will be no different.

That said, valuations remain elevated, geopolitical tensions persist, and the economic support we have relied upon in recent years is beginning to weaken. If a shock were to occur at this point, there would be fewer levers available to support the economy.

In this environment, we strongly favor a portfolio with a more defensive posture, one that positions clients to participate in the upside while helping to limit downside if conditions deteriorate. Given how our portfolios are constructed and how they have behaved in recent periods of stress, we believe we have struck the right balance.

Sincerely,

The BHPW Investment Team

Beverly Hills Private Wealth, LLC is a registered investment adviser. This is solely for informational purposes. No advice may be rendered by Beverly Hills Private Wealth, LLC unless a client service agreement is in place.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful. Past performance does not guarantee future results. Investing involves risk, including loss of principal. Consult your financial professional before making any investment decision. Other methods may produce different results, and the results for different periods may vary depending upon market conditions and portfolio composition. This newsletter does not represent an offer to buy or sell securities.